What Is Travel Insurance

Travel insurance is not a product you feel when everything goes right. You only understand its value when something quietly goes wrong — a missed connection in Chicago because of snow, a medical bill in Florida that your domestic plan won’t touch, or a last-minute cancellation due to a family emergency back home.

At its core, what is travel insurance comes down to one thing: transferring specific financial risks of travel to a policy that responds when timing, health, or logistics don’t cooperate. Not all risks. Not every inconvenience. Only the ones clearly written into the policy — and that distinction matters more than most travelers realize.

Why Travelers Misunderstand Coverage Before They Leave

Most people buy coverage late, skim the document, and assume protection is broad. We’ve reviewed enough denied claims to know where confusion starts.

Travel insurance does not function like health insurance. It does not automatically step in for every medical visit abroad. It responds to defined events, under defined conditions, during defined travel dates. If the policy starts after departure, certain benefits never activate. If an illness is pre-existing and not covered under a waiver window, claims stall. These details live in the fine print, not the brochure.

Understanding these mechanics early changes outcomes later.

What Does Travel Insurance Cover in Real Situations

Coverage is event-driven. Not emotion-driven.

Medical coverage applies when treatment is medically necessary and meets the policy’s definition of an emergency. We’ve seen claims approved for appendicitis in California and denied for follow-up therapy weeks later because the acute phase had ended.

Trip interruption coverage activates when a covered reason forces you to cut a trip short. A sudden hospitalization of an immediate family member qualifies. A voluntary decision to return early does not.

Trip delay coverage pays only after a waiting period and only for documented expenses — meals, lodging, ground transport — not inconvenience.

Baggage coverage reimburses depreciated value, not replacement cost, and only after airline liability has been applied first.

These are not technicalities. They are how policies are written and enforced.

Medical Evacuation Is Not Automatic Rescue

Medical evacuation is one of the most misunderstood benefits in travelers insurance.

Evacuation is approved when local facilities cannot provide adequate care — not when a traveler prefers treatment back home. We’ve seen evacuation approved from remote Arizona highways after severe trauma, and denied in major metro areas where equivalent care existed.

Transportation decisions are made by medical teams and insurers together, not by the traveler. The policy does not charter flights on request. It coordinates care when clinical necessity is established.

Understanding this distinction avoids false expectations during emergencies.

Timing Of Purchase Changes What Applies

When travel insurance is purchased matters.

Policies bought shortly after the initial trip payment often include time-sensitive benefits: pre-existing condition waivers, higher cancellation flexibility, and expanded medical terms. Policies purchased days before departure usually exclude these protections.

We regularly see travelers purchase coverage after symptoms begin, believing future complications will be covered. They are not. Insurance responds to unforeseen events, not developing conditions.

This is where planning, not price, protects you.

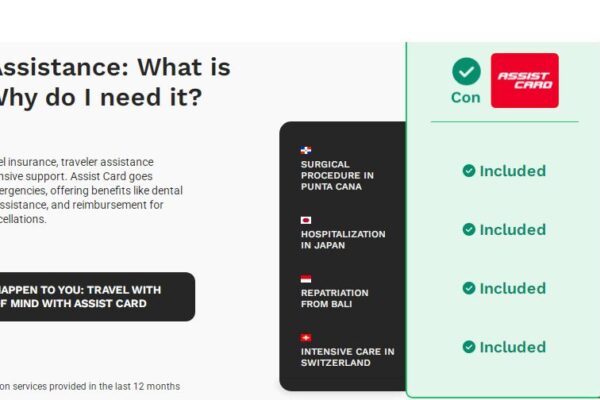

Credit Card Coverage Gaps Travelers Overlook

Many travelers rely on card-based coverage without reading its limits.

Credit card benefits often cap medical coverage at low amounts, exclude evacuation entirely, and require the entire trip to be charged to the card. Claims require extensive documentation and reimburse after the fact, not upfront.

We’ve seen card claims denied because a single hotel night was booked elsewhere. Travelers insurance policies do not hinge on such conditions.

Knowing the difference prevents expensive assumptions.

Claim Process Realities Most People Aren’t Told

Filing a claim is procedural, not adversarial — when documentation is complete.

Insurers require proof: medical records, physician statements, receipts, cancellation confirmations, and timelines. Missing documents delay processing. Inconsistent dates trigger reviews. Verbal explanations carry no weight without records.

This is not about distrust. It’s how insurance determines eligibility.

Travelers who keep paperwork, request hospital notes, and notify insurers early see smoother outcomes. Those who wait until after returning often struggle.

Is Travel Insurance Worth It For Domestic Travel

Domestic travelers often assume coverage isn’t necessary within the U.S. That assumption breaks down in specific situations.

Health plans may not cover out-of-network care at reasonable rates. Emergency transportation costs add up quickly. Weather disruptions cause cascading delays. Prepaid non-refundable bookings don’t adjust for emergencies.

Is travel insurance worth it? When a single interruption costs more than the policy itself, the answer becomes clear.

The value is not constant. It depends on trip structure, health considerations, seasonality, and destination infrastructure.

Is Travelers Insurance Good When Plans Change Suddenly

Travel rarely changes politely.

Illness doesn’t wait for return dates. Flights cancel without notice. Family emergencies don’t align with refund windows. Travelers insurance functions best when plans unravel fast and documentation exists.

It does not remove stress. It absorbs financial impact while decisions are being made.

That distinction defines its role.

Making Informed Decisions Before Departure

Travel insurance works exactly as written — no more, no less.

Understanding coverage before purchase, aligning benefits with real risks, and respecting exclusions leads to realistic expectations and smoother claims. This is not about buying more. It’s about buying correctly.

When travelers understand how policies respond in real conditions, outcomes improve. Fewer disputes. Faster resolutions. Clearer protection.

That’s how travel insurance is meant to function.